A single at-fault accident after age 65 can raise your premium 20-40% in Washington, but mature driver discounts and accident forgiveness programs can offset much of that increase. Here's how to find coverage that fits a retirement budget.

What Washington Drivers Over 65 Actually Pay After One At-Fault Accident

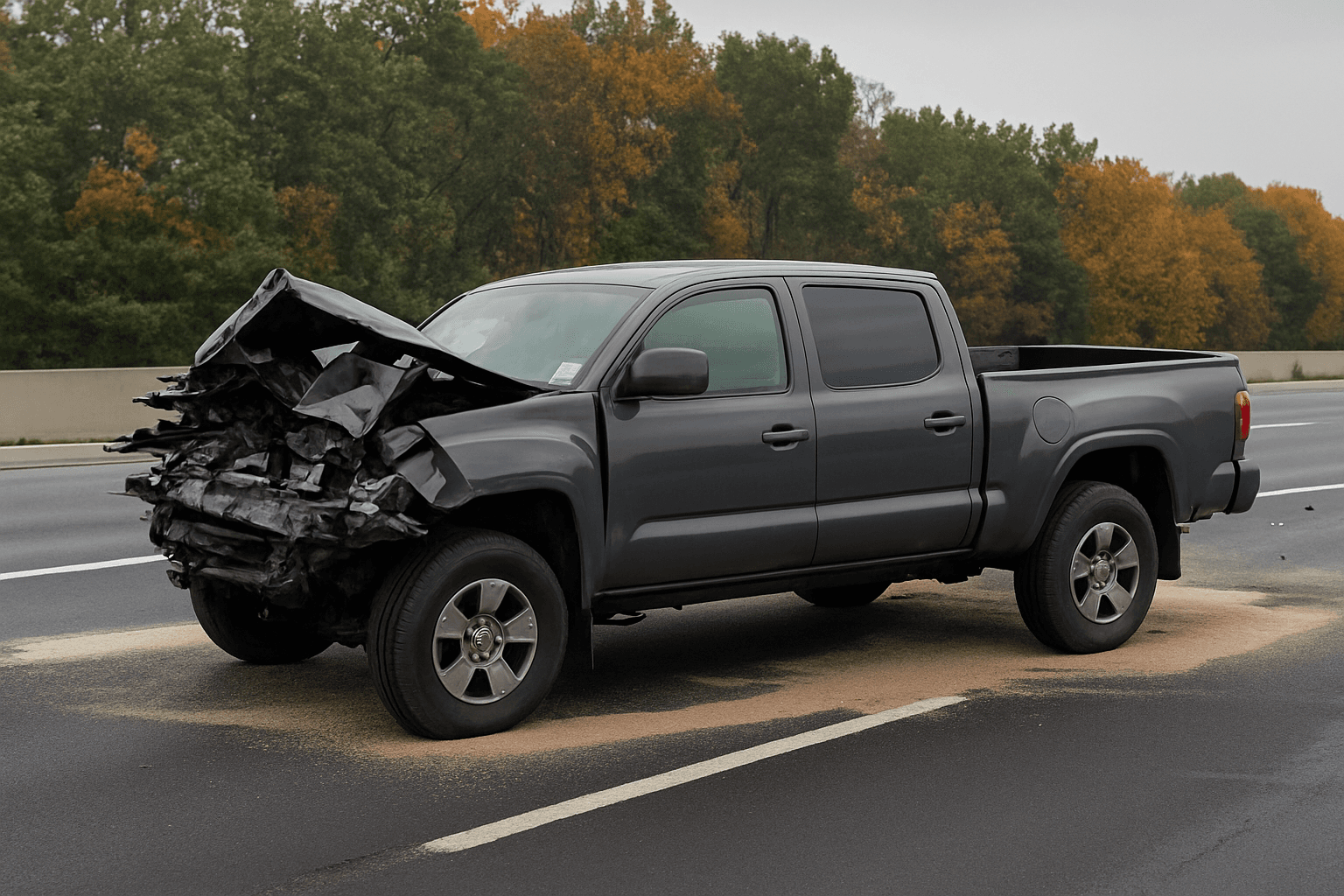

Washington drivers over 65 with a clean record pay an average of $75-$110 per month for full coverage. One at-fault accident raises that to $95-$140 per month, a 20-40% increase that persists for three years from the accident date. The surcharge varies by carrier and accident severity, with property-damage-only accidents triggering smaller increases than injury claims.

Washington operates as a pure comparative negligence state, meaning fault percentages determine liability split. If you're found 100% at fault, expect the higher end of the surcharge range. Carriers writing in Washington adjust rates based on claims history pulled from the Comprehensive Loss Underwriting Exchange, which tracks all claims filed in your name regardless of whether you switched insurers after the accident.

The accident surcharge is highest in year one and declines slightly in years two and three before falling off entirely. Most carriers recalculate rates at each renewal, so switching carriers during the three-year surcharge window rarely eliminates the increase. The exception: carriers offering accident forgiveness, which prevents the first at-fault accident from raising your rate at all.

How Washington's Mature Driver Course Discount Works After an Accident

Washington does not mandate mature driver discounts by statute, but most major carriers writing in the state offer them voluntarily. The discount ranges from 5-15% and requires completion of an approved defensive driving course designed for drivers aged 55 and older. The course must be retaken every three years to maintain eligibility, and the discount applies even if you have an at-fault accident on your record.

Approved courses include AARP Smart Driver (online and in-person, $25 for members), AAA's Driver Improvement Program, and National Safety Council Defensive Driving Course. All are 4-8 hours long and recognized by carriers writing in Washington. You must submit your completion certificate to your insurer within 60 days of finishing the course. The discount applies at your next renewal after submission.

The mature driver discount stacks with accident forgiveness where offered. If your carrier applies a 25% surcharge for the accident but you qualify for a 10% mature driver discount, your net increase drops to roughly 15%. Carriers don't automatically apply this discount at renewal. You must request it and provide the certificate. Industry estimates suggest 60% of eligible Washington seniors never claim it.

Compare rates from carriers that specialize in senior drivers

Mature driver discounts, low-mileage rates, and coverage reviews — see what you're actually eligible for.

Get Your Free Quote✓ Mature Driver Discounts✓ No Obligation✓ Licensed Carriers✓ All 50 States

Which Washington Carriers Offer Accident Forgiveness for Drivers Over 65

Accident forgiveness prevents your first at-fault accident from raising your premium. In Washington, this feature is offered by State Farm, Progressive, Allstate, Nationwide, and Travelers. Eligibility requirements vary: some carriers grant it automatically after five years of accident-free history with the company, while others sell it as an optional endorsement for $40-$80 per year.

State Farm and Allstate typically include accident forgiveness at no additional charge for long-tenured customers over age 50 with clean records. Progressive offers it as a paid add-on but often bundles it with their Loyalty Rewards program for drivers who've been with them three or more years. Travelers includes it in their Responsible Driver Plan for drivers with five consecutive years claim-free.

If you already had the accident, accident forgiveness won't remove the existing surcharge. It only applies to future incidents. But if you're shopping after an accident and expect to stay with a carrier long-term, choosing one that offers accident forgiveness protects you from compounding surcharges if a second accident occurs before the first one ages off your record.

Low-Mileage and Telematics Programs That Offset Accident Surcharges

Washington seniors who drive fewer than 7,500 miles per year qualify for low-mileage discounts with most carriers. The discount ranges from 5-20% depending on annual mileage and carrier. Progressive's Snapshot, State Farm's Drive Safe & Save, and Allstate's Drivewise use telematics to verify mileage and monitor driving behavior, offering additional discounts for safe habits like smooth braking and limited night driving.

These programs are particularly valuable after an accident because they discount based on current behavior, not past claims. If you drive infrequently and demonstrate cautious habits through telematics, you can offset 10-25% of your accident surcharge within the first policy term. Most programs require a smartphone app or plug-in device that reports data to the carrier for 90 days before applying the discount.

Combining a mature driver course discount, a low-mileage discount, and telematics rewards can recover $30-$50 per month of an accident surcharge. Carriers don't advertise this stacking potential clearly, and many seniors decline telematics programs assuming they're designed for younger drivers. The opposite is true: limited mileage and decades of driving experience produce the highest telematics scores.

Whether Full Coverage Still Makes Sense on a Paid-Off Vehicle After an Accident

Full coverage includes collision and comprehensive in addition to liability. After an accident, collision premiums rise because you've demonstrated claims risk. If your vehicle is worth less than $5,000 and paid off, dropping collision coverage can reduce your premium by $40-$70 per month, even with the accident surcharge applied to your remaining liability and comprehensive coverage.

Washington requires liability minimums of 25/50/10: $25,000 per person for bodily injury, $50,000 per accident, and $10,000 for property damage. Comprehensive coverage premiums are not typically surcharged after an at-fault accident because at-fault accidents don't predict comprehensive claims like theft or weather damage. If you drop collision but keep comprehensive, you still have protection against non-collision losses at a significantly lower total cost.

The break-even test: if your vehicle is worth $4,000 and your annual collision premium is $600, you're paying 15% of the vehicle's value each year to insure it. One more collision claim and you'll likely receive a payout below your deductible anyway. Most financial advisors recommend dropping collision on vehicles worth less than 10 times the annual premium. That threshold arrives sooner after an accident because the surcharge raises the collision premium faster than the vehicle depreciates.

How to Compare Rates Across Washington Carriers After an Accident

Washington seniors comparing rates after an accident should request quotes from at least five carriers, providing identical coverage limits and the same accident details to each. Rates vary by 30-50% for the same driver profile because carriers weigh accidents differently in their underwriting models. Some penalize property damage accidents lightly; others treat all at-fault accidents as equivalent.

Request quotes from both standard carriers (State Farm, Allstate, Farmers) and carriers that specialize in non-standard or senior markets (The Hartford, 21st Century, National General). The Hartford partners with AARP and offers accident forgiveness and mature driver discounts automatically for members over 50. They often quote competitively for seniors with one accident, even when standard carriers apply steep surcharges.

When comparing, confirm whether each quote includes the mature driver discount, low-mileage discount, and any telematics program discount you qualify for. Quotes that don't reflect these stacked discounts will appear 15-30% higher than your actual achievable rate. Ask each carrier explicitly whether accident forgiveness is included or available as an add-on, and factor that cost into your multi-year comparison.